Spot prices in Southern Norway are rising, with NO2 now leading as the most expensive price zone in the Nordics. What’s interesting is that this is happening despite hydro reservoirs sitting at seasonally high levels.

What’s driving the pressure? Southern Norway is facing a hydrological shortfall of around 10 TWh due to critically low snow accumulation. Without significantly wetter-than-normal weather this summer, reservoirs are on track to enter autumn and winter in deficit.

Even with support from Northern Norway, where hydro conditions are strong and power is in surplus, transmission bottlenecks limit how much help can realistically flow south. Flow-Based Market Coupling appears to prioritise the South, but it’s nowhere near enough to balance the books.

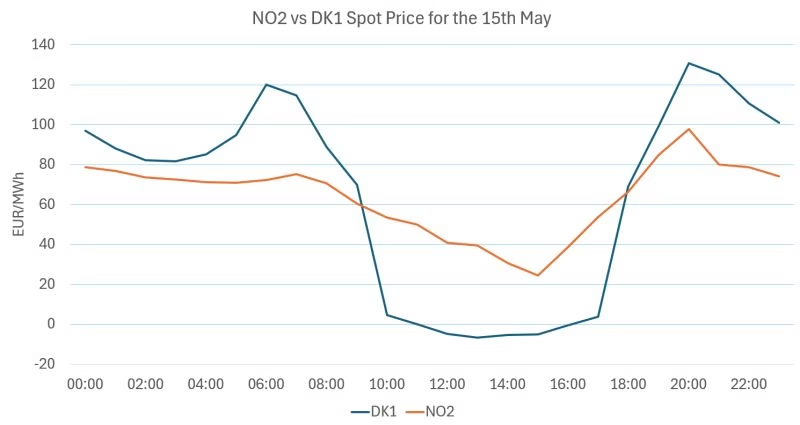

So where do prices go from here? We’re already seeing consistent imports during solar PV peak hours, yet prices in NO2 remain high. This results in six to eight hours of daily imports – but it’s not enough to stabilise the system in the face of a colder-than-average winter.

Looking ahead, we expect:

- A reduction in exports to Denmark – even outside solar hours.

- A rise in water values in NO2 to lift prices during off-peak.

- The NO2 spot price surpassing DK1 – and possibly Germany – once reservoir levels dip below normal. Based on current hydrological forecasts, we expect the tipping point to be in the first week of June.

The energy market in Southern Norway is entering a critical phase – and the price impact is just beginning.

See LinkedIn post here: https://tinyurl.com/rvwssrpk