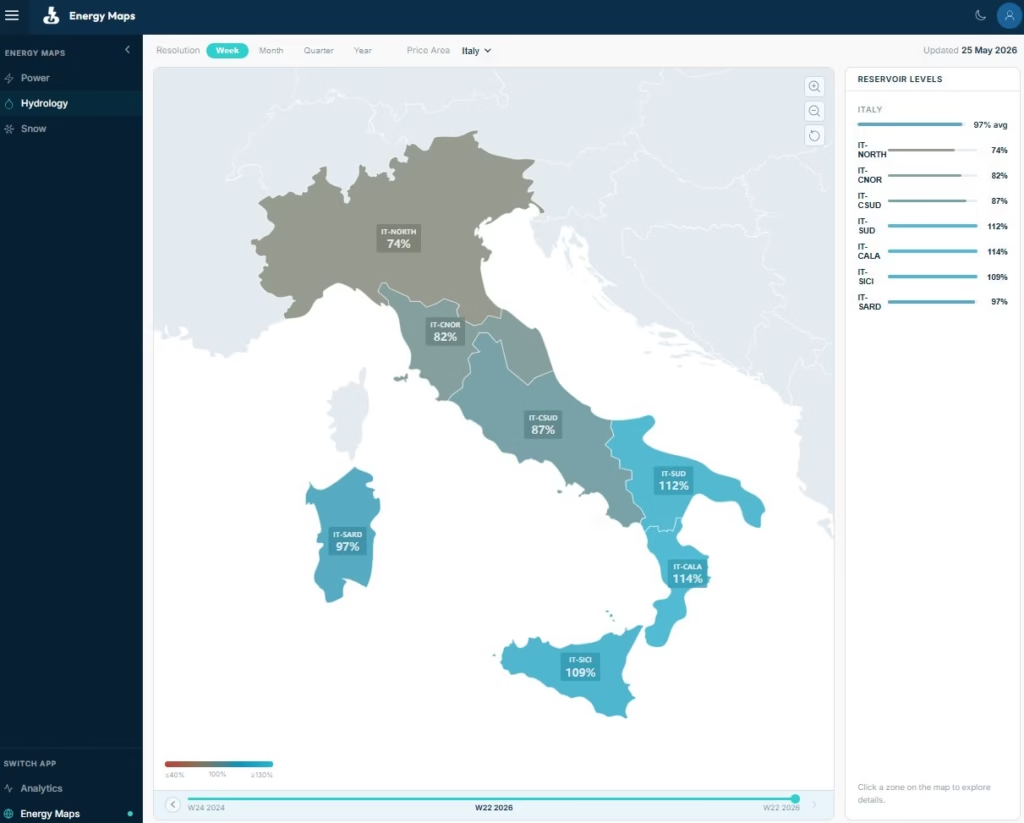

We’ve just added Italy to our hydro reservoir map – all seven bidding zones, tracked weekly as a percentage of seasonal normal.

The data reveals a sharp north-south split.

IT-NORTH and IT-CNOR

IT-NORTH – Italy’s largest hydro zone and the landing point for all cross-border imports from France, Switzerland, and Austria – sits at 82% of seasonal normal. IT-CNOR is at 84%. Both are below the median and still falling seasonally.

Southern Italy

The south looks very different. IT-SUD, IT-SICI, and IT-CALA are all at 100–112% of seasonal normal. A wet Adriatic spring has done its job there.

The surplus does not travel north. The main north-south transmission corridor is chronically congested, and all of Italy’s cross-border interconnections land in IT-NORTH. As a result, the driest zone is also the most exposed to the European price signal.

The Gas Market Matters Too

That price signal is under pressure. TTF is around €49/MWh, up 37% year-on-year, while the Strait of Hormuz remains effectively closed and EU gas storage levels are 15 percentage points below seasonal norms.

The Forward Risk

Alpine snowpack was already 48% below normal by late April (Drought Central Osservatorio Siccità, April update). The spring melt that normally refills IT-NORTH is nearly spent.

Less hydro heading into a tight gas summer means less of a buffer when it matters most.