Following the cold snap in early 2026, the hydrological deficit in NO2 has widened to around -13 TWh according to Norges vassdrags- og energidirektorat. Combined with other supportive factors, this has pushed up water values and, in turn, power prices in Southern Norway.

In our mid-term outlook, prices are expected to settle slightly above German prices for April, creating an unusual pricing situation. In the forward market, NO2 has switched to trading slightly below Germany for April.

The low reservoir filling levels are increasing the value of regulated hydropower. With limited risk of spillage, hydro producers can store water and optimise production, enhancing the strategic value of reservoir capacity.

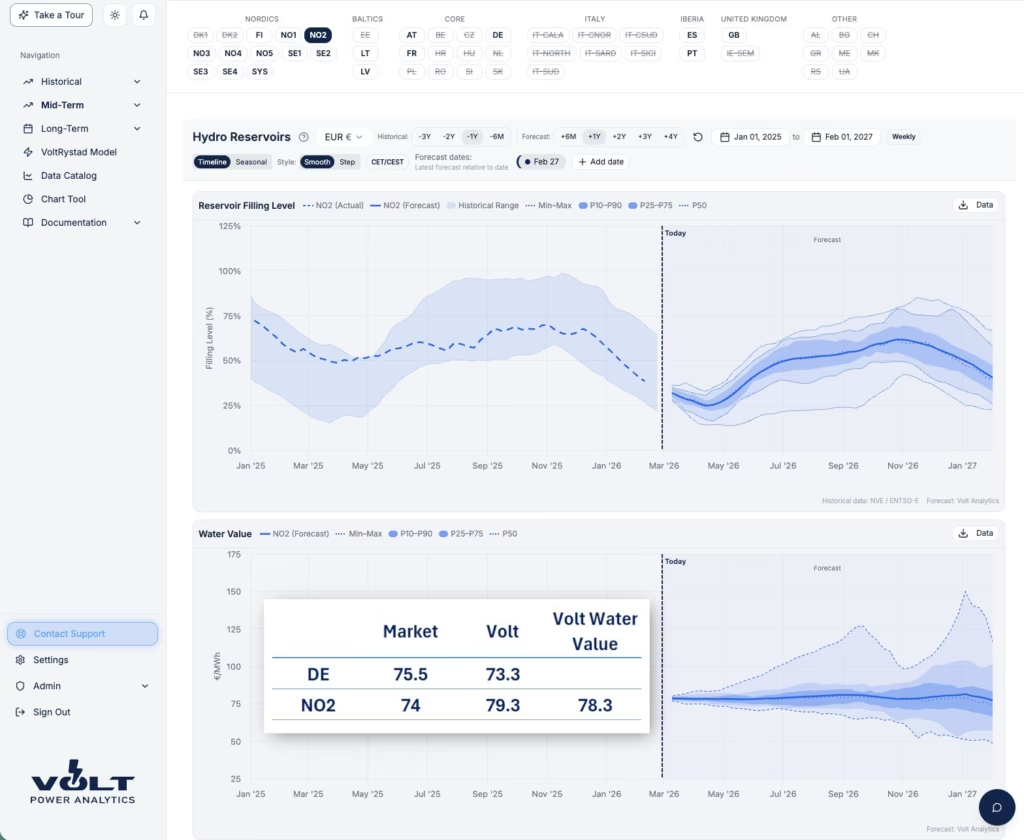

Reservoir levels in NO2 currently stand at 38.5%. During the same week in 2025, they were at 56.5%. By mid-April last year, reservoir levels were 49.5%. This year, we expect them to be significantly lower, averaging around 24%, with a simulated water value of EUR 78.3/MWh (both values are averages across our 30 weather-year scenarios).

In our most extreme mid-term scenarios, reservoir levels could fall to 14%, below the lowest level observed over the past 20 years of 15.2%. Water values across different weather scenarios show upside potential reaching EUR 84/MWh by mid-April.

The Outlook

Looking ahead, we expect spot prices in NO2 to remain above German prices during most daytime hours throughout the spring and summer solar season.

We also see limited risk of negative prices being imported from Germany and other continental price areas into NO2, as hydropower is likely to remain the price-setting technology in most hours during spring and summer.